Defence is no longer a defensive trade, and nowhere is the question of who's buying, who's building, and who is being left behind more apparent than in Australia, writes Professor Vince Hooper.

Markets, missiles and the end of the peace dividend — and what it means for Australia

A South Korean missile-maker most Western investors could not have located on a map two years ago has just hit an all-time high. LIG Nex1, a precision-guided munitions and electronic warfare specialist headquartered in Yongin, has nearly quadrupled from its January 2025 base, touching 899,000 won on 6 March 2026 — days after American and Israeli aircraft struck Iranian nuclear and missile facilities.

The Korean defence sector as a whole has returned roughly 137 per cent over the past year. These are not the numbers of a sleepy industrial cyclical. They are the numbers of an asset class being repriced in real time.

Defence is no longer a defensive trade. It is the trade. And nowhere is the question of who is buying, who is building, and who is being left in the queue more pointed than in Australia.

Canberra in the queue

For Australia, the arsenal trade is not an abstract market story. It is a mirror.

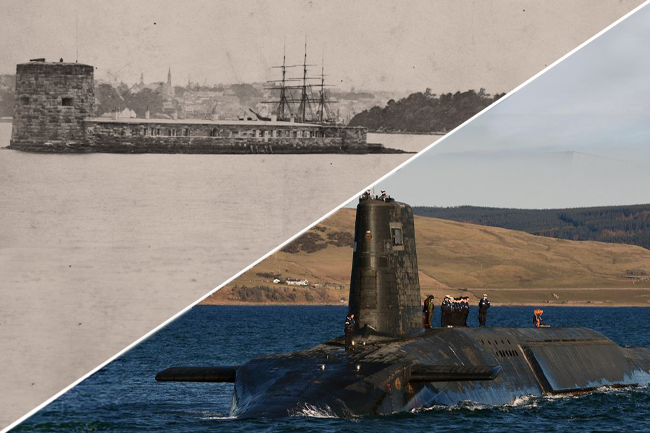

AUKUS is now a procurement queue rather than a strategy and the cost of waiting for Virginia-class submarines while the Indo-Pacific darkens is becoming uncomfortable to discuss in polite company.

Canberra is, in effect, paying premium prices for late delivery, while Korean and Japanese yards offer shorter timelines at lower cost.

Hanwha's confirmed 19.9 per cent strategic stake in Austal, cleared by both the Committee on Foreign Investment in the United States (CFIUS) and Canberra's Foreign Investment Review Board (FIRB) by late 2025, the Henderson shipyards build-up (now known as the Australian Marine Complex), the AS9 Huntsman self-propelled howitzer program being built by Hanwha at Avalon, near Geelong are not coincidences. They are the early signs of an Australian defence industrial base quietly rotating away from Anglosphere dependence and towards Asian arsenals that can actually deliver.

The strain is visible in real time. As the Sydney Morning Herald reported last week, Canberra's first crisis call during the Middle East escalation went to Beijing rather than Washington — a reflex inversion that would have been unthinkable a decade ago and that tells you more about the perceived reliability of the American guarantee than any AUKUS communiqué.

The ASX has noticed even if the cabinet has not: DroneShield, Electro Optic Systems, Codan and Austal have all attracted the kind of investor attention that only arrives when a market decides a sector's tail risks have permanently thickened.

From cost centre to industrial darling

The Ukraine War did the structural work. It converted defence from a politically awkward line item into the most fashionable corner of industrial policy and it taught Western treasuries an uncomfortable lesson about how thin their magazines actually were. Three years of artillery duels in the Donbas drained stockpiles NATO had quietly assumed would last a generation.

The Middle East conflict is the second shock. Patriot interceptors, Terminal High Altitude Air Defense (THAAD) reloads, Iron Dome Tamirs, SM-3s, 155mm shells, loitering munitions — each salvo over the Gulf is, in accounting terms, a revenue recognition event somewhere in Arizona, Alabama, Haifa or Daejeon. Governments that spent the 2010s running down inventories on the assumption of a benign world are now writing cheques to rebuild them, and they are writing those cheques into the same handful of balance sheets.

Who, specifically, is making money

Four tiers are visible.

First, the American primes — Lockheed Martin, RTX, Northrop Grumman, General Dynamics, L3Harris. They capture the replenishment contracts, the integration work, and the multi-year framework agreements that Congress now waves through with rare bipartisan enthusiasm. Their backlogs are at record highs and, after two decades of monopsony complaints, their pricing power has quietly inverted.

Second, the European awakening — Rheinmetall, BAE Systems, Leonardo, Saab AB, Thales. Germany's Zeitenwende turned out to be real, and Rheinmetall in particular has become the continent's de facto shell foundry, trading less like an industrial stock and more like a leveraged proxy on NATO's Article 5 itself.

Third, and most interesting from where Australia sits, the Asian arsenals — Hanwha Aerospace, Korea Aerospace Industries, Hanwha Systems and the LIG Nex1 of the opening paragraph, alongside Mitsubishi Heavy Industries and Kawasaki in Japan. South Korea has done what Europe spent 30 years failing to do: build a deep, exportable, price-competitive defence industrial base with delivery times measured in months rather than decades.

Warsaw noticed first. Riyadh, Canberra and Cairo are noticing now. Israel's own Elbit, Rafael and IAI sit alongside them as the technological pace-setters, particularly in air defence and electronic warfare, where the Iran exchange has been a brutal but effective live-fire showcase.

Fourth, the invisible compounders — the propellant chemists, the rare-earth magnet refiners, the speciality steel mills, the gallium nitride foundries, the International Traffic in Arms Regulation (ITAR) cleared software shops, the maritime insurers writing war-risk cover on Hormuz transits at multiples of last year's premium. This is where the quiet fortunes are being made. Lynas Rare Earths, sitting on one of the few non-Chinese heavy rare earth supply chains in existence, belongs in this tier, whether the market has fully priced it in or not.

The Gulf parallel

For the Gulf Cooperation Council (GCC), the calculation is different and more cynical than Australia's, but the underlying logic is the same. Every Gulf capital is simultaneously a customer, a forward operating base, and a potential target. Sovereign wealth is rotating accordingly — not away from defence, but into it. Saudi Arabia, in particular, is building domestic primes such as the Synchronised Accessible Media Exchange (SAMI) — wholly owned by the Public Investment Fund and openly targeting a place in the global top 25 defence companies by 2030.

The export of security capacity has become a new instrument of influence and the capital flows track the doctrine more faithfully than any white paper. Australia, with its Henderson precinct ambitions and its Hanwha partnership, is on a milder version of the same curve.

The uncomfortable coda

None of this is a celebration. A rising LIG Nex1 share price is, in the end, a market-implied judgement that more young people in more places will be killed by better-engineered weapons. The honest analyst names that trade-off rather than hiding behind the chart.

But the honest analyst also tells the truth about incentives. The Ukraine War did not enrich defence contractors by accident and the Iran strikes will not either. Governments that spent a generation treating deterrence as a sunk cost are now paying the bill they should have been paying all along and the firms holding the order books are, predictably, getting rich.

CNN reported over the weekend that U.S. intelligence believes China is preparing to deliver shoulder-fired air defence missiles (MANPADS) to Iran during the current ceasefire — a claim Beijing has formally denied. If the reporting holds, that single fact reframes the arsenal trade as an explicit great-power contest rather than a Western replenishment cycle — and it makes every defence ministry from Canberra to Riyadh recalculate how long it can afford to wait in the AUKUS queue.

For Australia, the question is sharper than for most. Canberra can keep waiting for Virginia-class boats and hoping the phone in Washington still gets answered, or it can do what Warsaw and Riyadh have already done — back the arsenals that can actually deliver, and accept that strategic autonomy in 2026 looks less like an alliance white paper and more like a procurement contract with Daejeon, Tokyo, Henderson or Geelong.

The post-Cold War peace dividend has been spent. What replaces it is already listed, already trading and already on the front page. The only open question is whether Australia is reading the same page as the rest of the market.

Professor Vince Hooper is a proud Australian-British citizen and professor of finance and discipline head at SP Jain School of Global Management with campuses in London, Dubai, Mumbai, Singapore and Sydney.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia License

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia License

Support independent journalism Subscribe to IA.