A practical guide for Australian SMEs building an insurance strategy across regulatory, cyber, and supply-chain disruption, covering broker selection and cover priorities.

Modern Australian SMEs operate inside a stack of overlapping disruptions. Regulatory tightening, cyber exposure, supply-chain volatility and telecoms reliability all reach the operational ledger at different points across the year. The insurance strategy question moves to the foreground when any one of those disruptions converts into a claim or near-miss event.

Australian SMEs working on their resilience plan sit inside that disruption stack. Specialist brokers like Morgan Insurance Brokers show the depth Australian operators should look for when reviewing cover. An insurance strategy is the deliberate alignment of cover, broker relationship and risk-management investment against the exposures the business actually faces. The decision rewards a few hours of structured preparation before the next renewal review.

Where are modern Australian SMEs most exposed?

Australian SME exposure has shifted meaningfully across recent years.

The most visible categories now include:

- cyber and data exposure reaching businesses of every size, not just enterprise targets;

- supply-chain disruption rippling through importers, exporters and even domestic operators;

- telecoms reliability gaps affecting any business that depends on phone, payments, or cloud services;

- climate-related property risk tightening insurer appetite across flood-prone, bushfire-prone and cyclone-prone postcodes; and

- workplace and director liability evolving alongside ASIC enforcement focus on management accountability.

The same kind of analysis visible in coverage of why Australia's mobile networks still depend on fibre translates to the broader resilience question. Each of these exposure shifts changes the cover the SME actually needs.

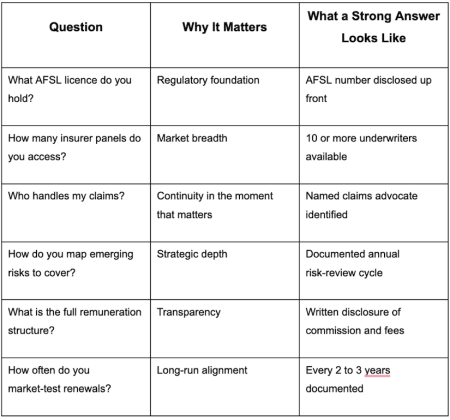

What should Australian SMEs verify in the first broker meeting?

The first broker meeting sets the tone for the relationship. The table below summarises six questions that surface the broker's depth and fit for the SME.

A broker that produces clear answers across these six points signals a partner worth retaining. A broker who deflects on any of them signals a generalist taking on SME work occasionally. The Australian Securities and Investments Commission's Moneysmart guide to insurance outlines the foundational framework Australian SMEs should reference.

Which risk categories pay off most from a specialist?

An Australian SME team discussing risk management strategy (Photo by Vlada Karpovich | Pexels)

Three risk categories meaningfully reward Australian SMEs working with a specialist broker:

- Cyber and data exposures where policy wording, notification obligations and incident-response support all interact with the realistic claim experience.

- Business interruption cover where supply-chain triggers, denial-of-access cover and indemnity periods all shape recovery from disruption events.

- Management liability and director-and-officer cover where personal exposure under Australian corporations law warrants specialist placement.

The Insurance Council of Australia's SME resources page outlines the broader framework Australian SMEs reference. The same kind of disciplined evaluation visible in coverage of why Australia's triple-zero service has faced repeated failures translates to the cover-and-broker decision. The first broker conversation typically runs 60 to 90 minutes covering operations, current cover and a written risk summary.

Where do Australian SMEs trip up?

A handful of recurring patterns produce poor outcomes for Australian SMEs after a claim. Recognising them in advance materially improves the realistic claims experience.

The most common errors include:

- renewing on the same broker without periodic market testing across alternatives;

- treating the headline premium as the primary decision factor rather than policy wording, sub-limits and exclusions;

- overlooking the claims-support pathway with brokers that disappear at the moments that matter;

- forgetting the cyber and management-liability gaps in traditional property-and-liability stacks; and

- signing without confirming the written remuneration disclosure under AFSL obligations.

Putting an insurance strategy together

The insurance strategy decision rewards Australian SMEs that plan rather than improvise. The window for thoughtful preparation runs from 60 to 90 days before renewal through to the broker-confirmation phase. The right broker coordinates the risk assessment, the market placement, the policy review and the claims support rather than treating each as a separate engagement.

Whether the SME operates in Sydney, Melbourne, Brisbane, Perth, Adelaide, or a regional Australian centre, the playbook translates cleanly. The first broker conversation should answer specific questions about market access, sector experience and claims protocol. Australian SMEs that run real comparison processes early end up with cleaner long-run outcomes than operators that default to whichever broker was first recommended.

Pre-engagement preparation pays back across the entire policy relationship. Annual reviews keep cover aligned with business growth, regulatory updates and emerging risks. The first conversation usually carries no fee or a modest engagement charge. Specialist Australian brokers like Morgan Insurance Brokers earn through commission on placed policies rather than upfront fees. Cleaner cover and faster claims outcomes typically more than offset the commission-versus-direct comparison for SMEs with meaningful operational exposure.

Australian SMEs that build the broker relationship into the operating rhythm land cleaner long-run outcomes. Quarterly check-ins on operational changes help. Annual cover reviews keep cover current. A market test every two to three years tests value.

The relationship matters more during the claim than during the renewal. Only a broker who has done the upfront work can advocate effectively when it counts.

Frequently asked questions

How often should Australian SMEs review their insurance strategy?

Review the full strategy every 2 to 3 years and run a renewal review annually. Major operational changes such as a new product line, an additional site, or a significant headcount shift typically warrant an interim review. The broker should flag market or regulatory changes that affect existing cover. Disciplined review cadence keeps cover aligned with reality.

What does cyber insurance typically cover?

Most Australian cyber policies cover incident response, notification costs, business interruption from a cyber event, ransomware payments where permitted and third-party liability. Policy wording differs meaningfully across insurers. Pre-incident specialist counsel often reduces both the realistic incident impact and the premium. Sub-limits and exclusions deserve careful review at placement.

Do brokers cost more than direct insurance purchase?

Most Australian brokers earn commission from the insurer rather than charging the SME a separate fee. The commission is embedded in the premium regardless of whether the SME goes through a broker or direct. The broker's role is to access more markets and negotiate better terms than the SME would achieve alone. Larger or more complex placements sometimes carry a separate broker fee disclosed in writing.

How do I know when to switch brokers?

Switch when the current broker stops market-testing renewals, when claims support falls short during an incident, or when the relationship fails to evolve with the SME's growth. A formal review every 2 to 3 years across two or three alternative brokers gives the SME a fact-based switching decision. Australian SMEs that test the market periodically typically secure cleaner long-run outcomes than operators that stay with the first broker indefinitely.