Self-professed finance and law maven Dominique Grubisa continues her deception, this time plagiarising an academic paper to make cases for her debt management service. David Donovan reports on the latest discovery in the Grubisa saga.

ONE OF THE SERVICES sold by Dominique Grubisa not yet covered by IA is her debt management service. Mrs Grubisa spruiks a service to erase debt in as little as six months without debt consolidation, debt agreements or declaring bankruptcy through her company, DGI Debt Management.

One client of DGI Debt Management was Barry from Western Australia. He was signed up to the debt management service and to Dominique Grubisa’s asset protection service featured in previous stories in IA. Barry featured in A Current Affair’s exposé on Grubisa in May of this year.

DGI Debt Management lodged a complaint on his behalf with the Australian Financial Complaints Authority (AFCA). As reported in the online article that accompanied the A Current Affair story, Barry claimed that DGI made up fake payout figures for non-existent loans and put fake documents to AFCA without his knowledge and consent.

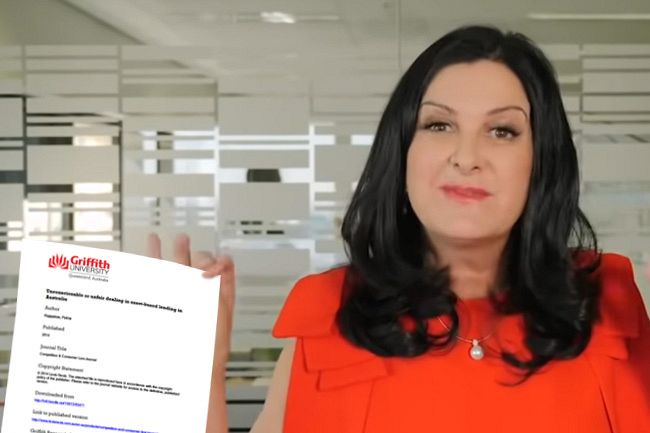

What didn’t feature in the ACA story was that DGI Debt Management plagiarised the work of Griffith University academic, Dr Pelma Rajapakse, in making arguments to his bank, Westpac. Paragraph after paragraph of DGI’s argument was lifted straight out of an academic piece penned by Dr Rajapaske published in the Competition and Consumer Law Journal in 2014. The article is also available on the Griffith University Research Repository.

DGI Debt Management argued Barry’s case saying:

Asset-based lending arises in circumstances where a lender provides a loan on the basis of security over an asset, rather than relying on the borrower’s capacity to repay the loan from their income. The more aggressive forms of asset-based lending will usually involve a lender taking security over the borrower’s substantial asset — in most cases this is the borrower’s primary residence, which has happened in the instant case. This will occur in circumstances where it is clear to the lender that the borrower has no capacity to repay the loan from their income.

Only the words in bold didn’t appear in Dr Rajapakse’s article.

They went on:

In such cases, there is a substantial risk that the borrower will default on the loan and lose their significant asset. These inappropriate practices have the potential to lead to unconscionable dealing and they have opened the door for unscrupulous lenders to engage in ‘morally repugnant’ lending practices.

The courts have discretion to grant relief and set aside a mortgage or loan agreement obtained because of the unconscionable conduct of a lender. Unconscionable conduct occurs where a borrower is at a special disadvantage and the lender knowingly takes unconscientious advantage of it.

In order to establish unconscionable conduct in equity, three elements must be satisfied:

1. The borrower must have been at a special disadvantage or disability with respect to the lender.2. The lender must have known or ought to have known of this special disadvantage.

3. The lender took unconscientious advantage of the borrower’s special disadvantage or disability.

Word-for-word from Dr Rajapakse’s article. Multiple further paragraphs followed all of which were lifted word-for-word.

The submissions put forward for Barry also made reference to alleged breaches of responsible lending obligations on the part of his lender. That would be fine had such obligations actually applied to his loan. Except they didn’t.

That the responsible lending provisions didn’t apply to Barry’s loan was something pointed out by Westpac to AFCA in a letter of 19 November 2020.

This prompted a question from AFCA to Barry’s then debt counsellor, Peta Lazarides:

‘The bank says that this loan was processed before responsible lending legislation was introduced. If you disagree, please explain why.’

Ms Lazarides responded:

‘The NCC came into force on 1 April 2010 and the loan offer was signed off on 15 April 2010.’

Barry took out his loan in 2010. The responsible lending provisions of the National Credit Code (NCC) didn’t apply to his lender until 1 January 2011.

AFCA also enquired regarding the association between Barry and the trust that had been set up as part of the asset protection product to which Barry had been signed up by Dominique Grubisa’s business.

In response to the question of what Barry’s association was to the trust, Ms Lazarides responded that the trust was a creditor of Barry.

Except the trust was not a creditor. Barry owed the trust not a cent, but this didn’t stop someone at Dominique Grubisa’s business from altering documents that he had completed genuinely and inserting figures for non-existent debts without his knowledge or consent.

So, who are these people at DGI Debt Management giving such fantastic advice?

According to an email sent to AFCA by Ms Lazarides, she is a ‘Wealth Creation Coach, Elite Property Mentor and Debt Councillor (sic)’.

Ms Lazarides’ Twitter accounts show she has broader interests. One account describes her as a ‘Consultant for positive change in small business. Opening entrepreneuriel (sic) minds’.

Her other Twitter account refers to ‘Personal transformation through Abundance Coaching, Crystal Resonance Therapy, Primus Activation Healing Technique, Reiki’.

A tweet from 2015, encourages her followers to ‘Stop charging your crystals. Clear them instead’.

If you are interested in understanding what that involves, you will find an explanation here.

There is nothing on Ms Lazarides’ Twitter posts to indicate she has any qualifications in law and certainly not any expertise in credit laws. Yet that hasn’t stopped her piling in with advice that was clearly wrong.

Barry also had the benefit of advice from a Sugandha Sehgal. Her LinkedIn profile refers to her being a ‘Credit Specialist at DGI Institute’ from September 2019 to August 2021. It also refers to her being a graduate of KLE Society’s Law College in Bangalore, India in 2019.

Despite Ms Seghal’s emails describing her as a credit specialist legal officer with an address in Sydney, Barry was not unsurprisingly shocked to find out Ms Sehgal was not qualified in Australian law and lived in India.

From 1 July this year, companies providing paid debt management services require a credit licence that authorises the provision of such services. At the moment, DGI Debt Management is operating under transitional provisions that allow it to continue to operate while an application for a variation of the credit licence by its related entity, DGI Finance, is considered by ASIC.

IA understands that Barry has made his concerns about the conduct of Dominique Grubisa’s business known to ASIC and the NSW Law Society.

As we always say when it comes to Grubisa — buyer beware!

You can follow founder and publisher Dave Donovan on Twitter @davrosz. Also, follow Independent Australia on Twitter @independentaus and on Facebook HERE.

Related Articles

- EXCLUSIVE: Lost for words, Dominique Grubisa resorts to plagiarism

- FAKE REVIEWS: More smelly catfish Vents for Dominique Grubisa and DGI

- EXCLUSIVE: Grubisa uses struck off solicitor parents to give legal advice to students and clients

- EXCLUSIVE: Equifax jumps ship after Grubisa starts distressing Uncle Sam

- IA's Dominique Grubisa investigation hits the mainstream

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia License

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia License

Support independent journalism Subscribe to IA.