A tradie can justify a $45,000 ute in five minutes, then spend five weeks guessing which finance structure will cost the least after tax, GST and interest.

That gap catches owners across construction, transport, hospitality and trades. They need the asset, but they do not want surprise fees, missed tax claims, or contracts stacked in the lender's favour.

The smartest choice depends on ownership, cash flow and timing. Get those three right and the asset should support growth instead of draining working capital.Key takeaways

The cheapest deal on paper is not always the cheapest deal in your business.- Choose finance by ownership, GST timing and cash flow, not by the advertised rate alone.

- Chattel mortgages suit assets you want to own long-term. Leases usually fit gear you expect to replace sooner.

- RBA data put average small-business lending rates near 7% per annum in early 2026, so compare fees, residuals and break costs too.

- The $20,000 instant asset write-off has been announced for extension to 30 June 2026, but confirm the law before you buy.

- Search the Personal Property Securities Register, or PPSR, on used assets and expect the lender to register security over financed equipment.

What asset finance is

This type of funding works best when the structure matches how the asset earns money.

Asset funding spreads the cost of a business asset across the period that asset produces income. Instead of paying cash up front, you match repayments to use.

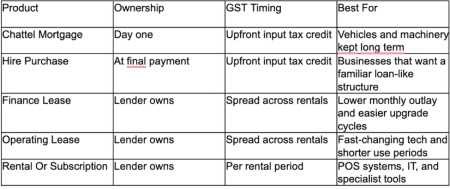

The main Australian structures are chattel mortgage, hire purchase, finance lease and operating lease. A chattel mortgage gives you ownership from day one. Hire purchase transfers title at the last payment. A finance or operating lease leaves ownership with the lender.

Approval usually depends on your ABN, GST registration, Business Activity Statement history, bank statements and the asset's type and age. Small-business loans usually sit outside consumer responsible lending rules, but unfair contract term laws still matter.

If you are GST-registered, you can usually claim input tax credits on business-use purchases. Cars are subject to the ATO car limit of $69,674 for 2025-26.

Three big benefits of asset finance

Used deliberately, asset finance can protect cash, improve tax timing and keep growth moving.

Preserve cash flow and match costs to use

Matching the term to the asset's life protects working capital. A 48 to 60 month term with a 20 to 30% balloon, meaning a larger final payment, can keep monthly costs steady on utes, trailers, or workshop machinery. Seasonal repayments can also help businesses with uneven income.

Use tax deductions correctly

Assets under $20,000 may qualify for the instant asset write-off if the 2025-26 extension becomes law and the asset is first used or installed on time. Otherwise, you depreciate the asset. With a chattel mortgage or hire purchase, GST credits are usually claimed upfront. With leases, GST is claimed across each rental.

Move faster without giving up protections

Non-bank lenders and brokers can approve straightforward deals quickly with low-doc checks. That speed helps when stock is limited, but it should not stop you from reading the contract. From 9 November 2023, unfair terms in standard-form small-business contracts can attract penalties, so challenge one-sided indemnities, broad default clauses and lender rights to change terms whenever they like.

Which structure to choose

Start with ownership, asset life and tax timing, because those three factors shape the real cost.

Ask three questions. Do you need ownership, how long will the asset stay useful and when do you want GST credits and deductions to hit?

Watch the end of the deal, not just the monthly payment. Lease residuals, which are the end-of-term amount tied to expected value, must meet ATO minimums. Rentals can be simple, but auto-renewal and damage clauses deserve a close read.

Where to apply for a fair deal

Competition is still the easiest way to improve price and contract terms.

If you want one point of contact to benchmark lenders, compare fees and shape a deal around your cash flow, especially when you are weighing a chattel mortgage with a 20 to 30% balloon on a 60-month term, an independent broker such as Switchboard Finance may help with fast low-doc assessment, same-day quotes and equipment finance for ABN and GST-registered businesses trading 12 months or more.

Get at least two lender quotes and one broker benchmark before you sign. Compare total cost, fees, end payments and security requirements, not just the rate.

Major banks can price well for strong borrowers, but approvals are slower and security can be broader. Non-bank asset financiers are usually faster and more open to used or niche equipment, though documentation and fees can be tighter.

A broker can save time if they show real lender options and explain the trade-offs clearly. If you speak with a specialist such as Switchboard Finance, ask how many lenders they will approach, whether same-day quotes are realistic for your profile and what fees they earn.

Vendor finance can look convenient, especially on low-emissions vehicles or energy-efficient gear backed by Clean Energy Finance Corporation programs. Still, compare it with outside quotes so a discount on the sticker price is not hiding a higher finance cost.

How to track ROI

A financed asset should add more profit or savings than it costs each month.

Approve equipment only when extra gross profit or cost savings beat the monthly repayment, running costs and a repair buffer. A simple test is: added gross profit minus finance cost minus maintenance reserve equals monthly net gain.

If the asset may qualify for the instant write-off, add the tax effect to your first-year view. Then stress-test the deal with interest rates two points higher and two points lower. If the numbers only work in the best case, wait or negotiate harder.

Make finance work for you

A good finance structure should support profit, not pressure your cash.

Treat asset funding like any other capital decision. Match the structure to the asset, protect cash flow and use competition to improve price and terms.

A ute, mixer, lathe, or server should earn more than it costs. When the contract is fair and the numbers are clear, finance becomes a tool instead of a drag.

FAQ

These answers cover the issues that usually trip up first-time borrowers.

What is the difference between a chattel mortgage and hire purchase?

They are similar in economic effect. With a chattel mortgage, you own the asset from day one. With hire purchase, title passes at the last payment. Both can allow upfront GST credits for business use, subject to the ATO car limit.

What rate should I benchmark in 2026?

RBA data showed average small-business lending rates of 7.03% per annum on outstanding loans and 6.91% per annum on new loans in February 2026. Use those figures as a check, not a promise, because pricing still depends on risk and security.

Can I instantly write off multiple assets?

Yes, if each asset is under the per-asset threshold and the law is in force for that income year. Each asset must also be first used or installed by the deadline. Check the ATO position before relying on the announced extension to 30 June 2026.

What is PPSR and why does it matter?

The Personal Property Securities Register is Australia's record of security interests over non-land assets. Lenders register their interest over financed equipment. When you buy used equipment, search PPSR first, so you do not inherit someone else's problem.

Where can I complain if a lender treats me unfairly?

Start with the lender's internal dispute process. If the lender belongs to the Australian Financial Complaints Authority, or AFCA, you may be able to escalate there. For AFCA purposes, a small business generally means fewer than 100 employees.